|

Getting your Trinity Audio player ready...

|

Investing and getting insurance as a tran or non-binary person may be easier than you think. I’ve talked with several folks who fear that it’s not available to them, so they brush it off, but I’m here to say that’s not the case.

Investing

Investment account applications typically require certain identification details such as:

· Name

· Date of birth

· Social Security Number

· Marital status

When investing with my broker/dealer, all of our account applications require applicants to use their legal name, which is basically what is listed on your Social Security card. The reasoning is that all our applications go through an identity checking system that matches people’s identifiers with a national system that proves you are who you say you are, which is a fraud-prevention measure. Perhaps not all companies have the same requirements. Personally, I feel safer knowing that the investment company I work with prioritizes protecting my identity, but if this doesn’t feel right to you, then you might consider checking around to see how others do it.

Life Insurance

Let’s now address life insurance. You can get life insurance through the same avenues as a cisgender person. The process will likely be a little more involved, but nonetheless, it is possible. It starts with investigating insurance companies.

Before we delve into the details, let’s go over the basics of life insurance. There are two main ways to apply for it. One way is to apply for a guaranteed-issue plan that will not require any underwriting in order to insure you. These policies are often quite expensive because they are not based on any risk-based information other than your age and the benefit amount you’re applying for. The other way is to go through an underwriting process, which requires more information which is used to best determine your insurability and premium cost. All underwriting policies will need the same information to properly underwrite someone’s risk:

· Age

· Gender (often required)

· Occupation

· Blood pressure

· Build (height and weight)

· Cholesterol

· Physical health history

· Mental health history

· Surgical history

· Family health history

· Prescription history

· Chronic health conditions

· Tobacco use

· Illegal drug use

· Driving record

· Criminal record

· Bankruptcy history

· Travel to dangerous countries

· Participation in high-risk recreation

You’ll note that Mental Health is listed above. This includes evaluation for issues such as depression and/or suicidal ideation and attempts—both of which are prevalent in the LGBTQ+ community, especially for our transgender clients. Insurance companies are less likely to insure someone with a suicide attempt within the past two years or a hospitalization for a mental disorder within the past year, according to Qualifying for Life Insurance When You’re Transgender, Investopedia.com. Not all insurance companies underwrite mental disorders (such as depression) the same. There are plenty of insurance carriers that have rated people with a history of depression as the highest health rating. It just depends on the carrier. Regardless of past history, note that all life insurance policies have a suicide clause which makes the policy null and void if suicide occurs within the first two years of the policy.

As part of the physical health history evaluation, all life insurance applicants must go through many different tests, including HIV testing. I once was questioned by a lesbian couple why this was part of their underwriting process, as they felt targeted. They were unaware that this is required of all applicants—straight, gay, bi, transgender, cisgender, etc. Do not let this alarm you, everyone goes through HIV testing when applying for life insurance.

What’s not shown on the list above, but is required by most insurance companies, is your gender. This may seem inconsequential, but gender can be an important factor in determining risk as it has historically been correlated with one’s life expectancy. For instance, since 1880 there has been a worldwide historical relationship between being male and having a shorter life expectancy, according to Provisional Life Expectancy Estimates for January through June, 2020, Vital Statistics Surveillance Report. According to the CDC, a child born male in 2020 has the life expectancy of 75.1 years while a child born female in 2020 has a life expectancy of 80.5. While it’s generally required by all insurance companies to use gender in underwriting, it’s unfortunate that there is no uniform practice, or standard, for how this information will be used in the underwriting process. Some companies will underwrite you based on the sex assigned at birth while others will use your true gender. Some insurers’ requirements differ depending on the length of time you’ve been undergoing any hormone therapies or the duration of time passed since any gender affirming surgeries.

My broker/dealer is affiliated with a well-known life insurance company in the top five of the nation. For life insurance this company has applicants apply using the gender they identify with. If you are non-binary then they have you go through underwriting using the gender you were assigned at birth. This is true of several other insurance companies, but not all. To save you the time researching the marketplace, instead, you could choose to work with an advisor that is familiar with this area. Not only will you be guided through the process by someone who is familiar with it but you have a built-in advocate should you come across any issues or concerns.

Disability Income Insurance

Similar to life insurance, not all insurance companies underwrite the same way. Many of the factors used to determine insurability for disability income insurance are also used for long term care insurance, which are outlined below. This is because disability income insurance is covering a different risk other than death as there aren’t any benefits paid at death, but instead are paid in the case of a disability. This means they are concerned with your job (is it hazardous?) your hobbies (do you enjoy rock climbing or skydiving?). They’re looking for something in your life that is likely to cause you to make a claim with them. When underwriting for disability income insurance, some companies have unisex rates so gender isn’t a factor. For those that don’t, many will underwrite using your true gender and only a handful will underwrite using the sex assigned at birth. For someone who is non-binary, the underwriting process would use the gender assigned at birth. Many of the carriers are not concerned with hormone therapy, though a few need a history of six months of use without complications. As for gender-affirming surgery, this is also a non-issue to many insurance companies, though a few require a 90-day wait period after the surgery to ensure there aren’t any resulting issues, as they would with any surgery, according to Crump Insurance brokerage service.

Long Term Care Insurance

At this time, none of the carriers I have access to will underwrite using your true gender. Some use birth-gender while others will use the gender you have transitioned to, but only if you’ve undergone gender-affirming surgery.

Essentially, the data points asked in underwriting long term care insurance are different than those of life insurance because the insurance is covering a different risk other than death. They are concerned with a diagnosis or disability that causes you to be unable to perform two out of the five Activities of Daily Living, such as bathing, getting in and out of bed or a chair, feeding yourself, toilet hygiene, getting dressed, personal hygiene, walking/climbing stairs, and safety/emergency responses. Naturally, the information they need to properly insure this risk will be slightly different. The information needed for a long term care insurance application are:

· Age

· State of residency

· Marital status (married or unmarried)

· Gender (often required)

· Build (height and weight)

· Physical health history

· Mental health history

(specifically for psychiatric/psychological disorders)

· History of Diagnoses

(several common diagnoses are an automatic decline)

· Prescription history

· Chronic health conditions

· Tobacco use

· Current health concerns

· Current physical health/limitations

· Surgical history (Including gender reassignment surgery. If yes, were there any complications.

If no, do you plan to undergo such surgery?)

· History of drug or alcohol abuse

· Hormone or psychotherapy treatments

(If yes, when did therapy begin?)

As shown, not only do insurance companies underwrite differently, but there are also many different types of long term care insurance products available. At this point, you might be discouraged knowing most long term care insurance carriers will only underwrite an individual based on the gender they were assigned at birth. But there might be a work-around for this. As mentioned previously, several life insurance companies, including the insurance company connected to my broker/dealer will underwrite you with your true gender. That being said, let me introduce you to the hybrid life insurance policy. The base is a life insurance policy that works like any other permanent life insurance policy as it has cash-value and offers a death benefit. Then, on top of that, it includes a long term care rider, which uses the life insurance benefit for long term care, if needed. It’s really a fantastic way to cover two needs at once, as well as offer a way to be insured in a more authentic way.

Hopefully any questions you’ve had are now answered, and you now feel more confident about investing and insurance. It’s not uncommon for most new investors to have fear, but it shouldn’t be due to fear of rejection or judgment. There are plenty of other issues in life that are worth worrying over, but this should not be one of them. By arming yourself with partnerships within the industry you can be confident that the steps you end up taking are right for you. And really, that’s all that’s important in this world—doing what’s right for you. And when it comes to financial matters, I believe the best way to start is to find an advocate who is seasoned in the industry, and together you start by biting off one bite at a time. This way you will feel comfortable asking as many questions as you need to ask, and can begin building your financial foundation both empowered and prepared.

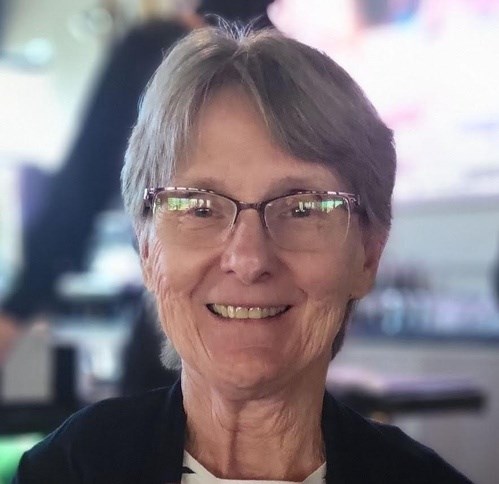

Carrie Waters Schmidt, MS, CFP®, AWMA®, ADPA®, CSRIC is the Founder of Equanimity Wealth Planning and Investing in Madison. She is an Ally and advocate for the LGBTQ+ community. She is dedicated to ensuring everyone has a place in the investment markets and is committed to keeping you on your path to success. CRN-4293382-020822

0 Comments